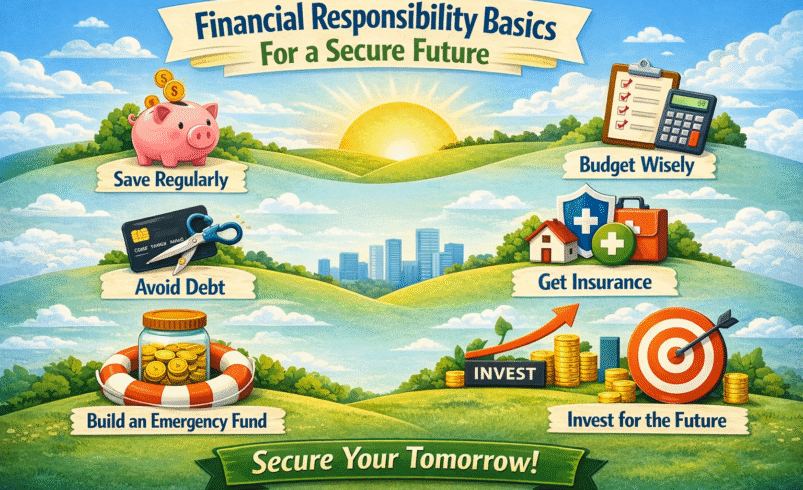

Financial Responsibility Basics For a Secure Future

- December 27, 2025

- 0

From managing personal obligations to navigating the ever-expanding to-do lists that seem to define our days, each of us is sustained by life’s hustle, So, finding the time

9621 Agnes Crossing, Lake Suzanneview, New Mexico Island 84604-9295.

From managing personal obligations to navigating the ever-expanding to-do lists that seem to define our days, each of us is sustained by life’s hustle, So, finding the time

From managing personal obligations to navigating the ever-expanding to-do lists that seem to define our days, each of us is sustained by life’s hustle,

So, finding the time to properly arrange our finances can seem like a daunting addition to an already hectic agenda. However, delaying this critical preparation can result in missed opportunities to secure a healthy financial future.

Once you become financially responsible, you can provide comfort and relief from financial stress in an era when economic issues such as inflation and rising living costs persist.

Recent figures highlight the urgency.

According to a reliable survey, 33% of Americans have more credit card debt than emergency savings in 2025, which is a slight decrease from previous years but still high due to earlier inflation pressures.

Additionally, 59% of Americans are unable to pay a $1,000 unexpected cost with only their savings, commonly resorting to debt or borrowing. You can also develop healthy habits early on to help you avoid these issues and attain financial stability.

As a result, in this guide, we will discuss why financial responsibility is important, its principles, and how to manage it.

Financial responsibility can be defined as making informed decisions about income, spending, saving, investing, and debt management. Furthermore, it is critical for individual and community well-being.

In this era of intricate financial goods, rising costs, and economic unpredictability, it allows people to achieve stability, reduce stress, and establish long-term security.

In addition, work consistently shows that financial responsibility leads to increased financial well-being. Whereas irresponsibility refers to debt cycles, mental health problems, and economic vulnerability.

The primary principle of financial responsibility is to spend less than you earn. So, this reduces the accumulation of high-interest debt and makes room for savings.

What you need to do is to track your income and expenses to ensure that the necessities are met first.

Budgeting is vital for financial management. The 50/30/20 guideline is one of the popular methods:

So, set aside 50% of your income for essentials (housing, food, utilities), 30% for wants (entertainment, dining out), and 20% for savings and debt reduction.

Moreover, you can also use apps or spreadsheets to track your expenditure and make adjustments as necessary.

Always recall, life is uncertain. According to experts, you save 3-6 months’ worth of living expenses in a liquid account. By 2025, 27% of Americans will have no emergency savings.

So, always aim to start small, aiming for $1,000 at first and working your way up.

Now you need to prioritise high-interest debts, such as credit cards, by employing debt avalanche (highest interest first) or snowball (smallest balance first for motivation).

Avoid incurring additional debt by paying bills on time and maintaining credit utilisation below 30%.

You have to automate contributions to your retirement accounts, such as 401(k)s and IRAs, particularly to catch company matches.

You will need to diversify your investments, including equities, bonds, and index funds, for long-term gain.

You need to create a plan and regularly contribute to tax-advantaged accounts before retirement. So, consider inflation and healthcare expenditures. Online calculators, for example, can assist you in estimating your demands.

Lastly, you have to stay informed with books, courses, and consultants. Because financial literacy enables smarter judgments.

In today’s economic climate, financial stewardship is more important than ever. U.S. household debt is likely to exceed $18.6 trillion by late 2025 (averaging more than $105,000 per home), with personal savings rates staying around 4.5-4.8%.

Many Americans are struggling with growing expenditures, high interest debt, and unanticipated bills. Yet, developing good habits can lead to increased security, less stress, and long-term wealth accumulation.

Here are the practical tips for handling financial responsibility.

A budget is the basis for financial responsibility. So, monitor your income and expenses to ensure that you are living within your means.

There is a popular technique that you can use 50/30/20 guideline (50% needs, 30% wants, and 20% savings/debt reduction).

Here are some tips you can utilise.

You need to think about unexpected events such as job loss, medical expenditures, or care can wreck finances if there is no safety net in place. Set aside 3-6 months’ worth of essential living expenditures in a high-yield savings account.

Always remember that debt can quickly spiral out of control, especially with credit cards with interest rates higher than 20%.

As a result, once you take financial responsibility does not imply poverty; rather, it means delegating yourself and creating a future in which money works for you.

Further, budgeting intelligently, saving diligently, managing debt, and investing thoughtfully can help you attain long-term stability and minimise stress.

So, begin today with small, consistent actions that accumulate over time, resulting in greater freedom and opportunity tomorrow. Your secure future begins with the decisions you make today.