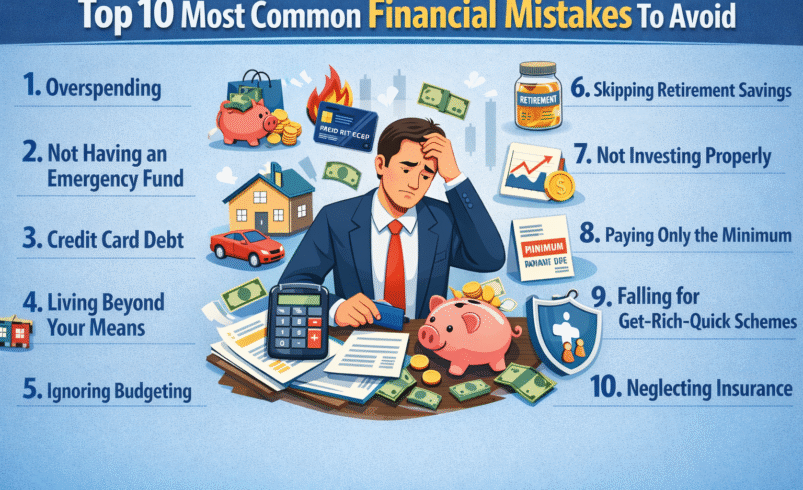

Top 10 Most Common Financial Mistakes To Avoid

- December 29, 2025

- 0

Not everyone understands everything right away in life. Many people take the effort to learn how to manage their money properly. People spend money in very diverse ways,

9621 Agnes Crossing, Lake Suzanneview, New Mexico Island 84604-9295.

Not everyone understands everything right away in life. Many people take the effort to learn how to manage their money properly. People spend money in very diverse ways,

Not everyone understands everything right away in life. Many people take the effort to learn how to manage their money properly. People spend money in very diverse ways, even when they live the same way. So, it’s true that hardly anyone becomes financially stable at a young age. A lot of the time, they make the same financial blunders.

Even tiny, frequent costs can mount up over time and hurt your overall financial health, especially if you use credit cards. Interest that builds up makes things even harder.

On a bigger scale, spending too much on significant things like cars and homes might make it hard to keep track of your money.

We’ll talk about bad financial choices that people often make in this article. We know that things happen in life, like getting into debt.

If that happens to you, these 10 tips can help you make things easier. Look through this list to uncover ways to improve and keep your financial health.

It’s easy to spend too much and not know where your money is going if you don’t keep track of your income and expenses. Surveys suggest that not making a budget is one of the biggest regrets, which can lead to debt and stress about money.

Many Americans regret having credit card debt because the hefty interest rates (over 20% on average) make it hard to pay off. It keeps people stuck in a cycle of making the least amount of payments.

Small daily costs, like eating out and subscriptions, add up. For example, $25 a week on lunches is $1,300 a year. This means you have to live from one pay cheque to the next.

When you buy something big, like a new car, you lose 10–20% of its worth right away and have to make high payments.

Unplanned costs, such as medical bills or losing a job, can make you depend on high-interest loans. In 2025, about 40% of Americans will wish they had saved more money. Bankrate says that many people have less than three months’ worth of expenses saved.

If you don’t have enough health, life, or disability insurance, you could end up paying a lot of money for medical care or accidents.

Following trends (such as meme stocks) or being too patient can be a waste of time in the market. Emotional decisions, such as panic selling, hurt returns.

Repeatedly, those who lack financial literacy repeat the same mistakes. Research from FINRA shows that a lot of people overestimate their knowledge.

Tax season is a stressful and difficult period for saving money because of missing deductions or receiving unexpected bills.

The power of compound interest is lost if one does not begin early. With employer matches no longer an option, many people wish they had started saving for retirement earlier.

Envision yourself taking a nap each morning, secure in the knowledge that you have an emergency fund and no debt to worry about. Plus, the satisfaction of watching your savings pile up for the retirement of your dreams.

The other side of these common blunders is a life where opportunities, not constraints, are paramount. As the year 2025 winds down, remember that about 80% of individuals feel some kind of regret. In any case, you are now equipped to end that pattern.

Achieving financial independence is more important than being perfect. Whether it’s paying more than the minimum on your credit card, keeping a spending log for a week, or automating a $50 transfer to your savings account, make one small change today.

Not only are these things that need fixing, but they are also the foundation for a future where your money works for you.

I have faith in you. You need to turn the “what ifs” into “I’m glad I did.” Thank your calmer, wealthier self in 2026. Season’s greetings! Wishing you a successful one.